CRYPTO CYCLE IS BOTTOMING

PUBLISHED: 2026-09-07

CATEGORY: Market Analysis

Bitcoin remains in deep value after five months below key investor cost bases. Long-term holder capitulation is accelerating while ETF flows stay negative. Derivatives have de-risked but the options surface retains a defensive tilt. The bottoming process is advancing, but not yet complete.

As we wrote previously, second leg down took place in June, as we believe this month may have a rally relief, however at the end of summer into fall we may have the final leg lower which will bring the true bottom of the cycle.

1. current situation in brief

Bitcoin remains in deep value territory after five months below the True Market Mean and Short-Term Holder Cost Basis, with long-term holder loss realization now accounting for 43% of total realized value and peaking at $280M per day, the highest since December 2022.

ETF netflows have eased but remain in net outflow, while daily trading volume at $650M–$950M sits approximately 80% below the October 2025 peak, confirming institutional demand has not stabilized.

Derivatives positioning has shifted cautiously long with the put/call ratio at the lowest reading in 2026, yet the options surface retains a defensive skew and spot trades well below max pain, leaving the market in the later stages of a bottoming process where sustained cooling in LTH capitulation is the key condition for recovery.

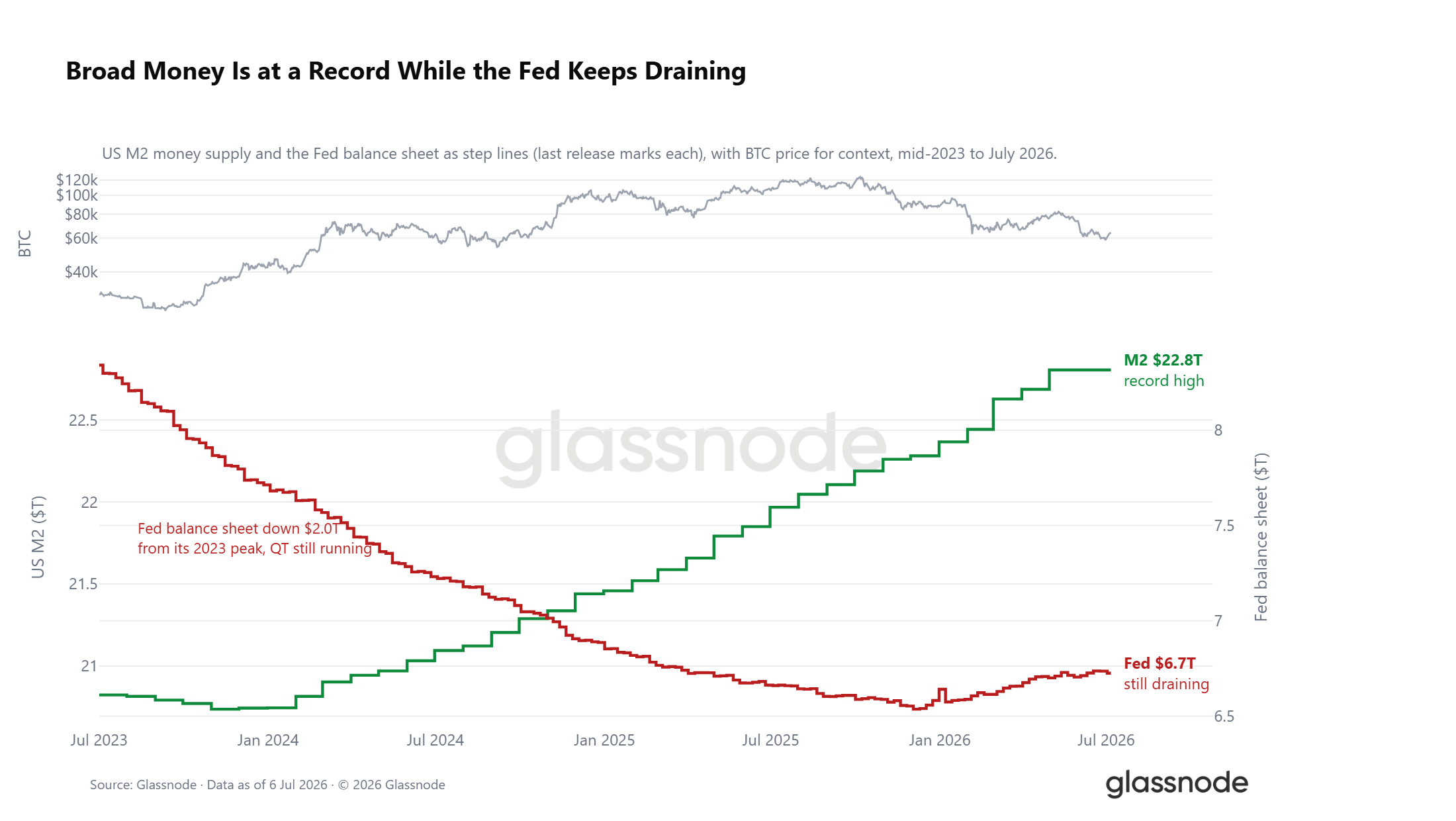

2. Liquidity situation

Underneath the shock, the liquidity backdrop is split. US M2 has pushed to a record $22.8 trillion, the slow tide that has historically led risk appetite, yet the Federal Reserve's balance sheet keeps draining, now $2.0 trillion below its 2023 peak. The tension is a rising broad-money base set against an ongoing quantitative drain, with real yields still near 1% keeping the cost of holding a non-yielding asset high. The macro door is not shut, but it is not yet firmly open.

As we expect the rates not to increase this leads to increasing appetite for scares assets like gold, silver and BTC in the future. If rates go down this will bring real yields to 0% territory which at the same time brings money to scares assets.

3. ONCHAIN DATA

Bitcoin has bounced from $58.3k to $64.4k over the past week, a constructive near-term development but one that leaves price firmly below both the True Market Mean at $76.6k and the Short-Term Holder Cost Basis at $72.2k. Until these levels are reclaimed, the market remains in deep value territory and structurally vulnerable to any external negative catalyst. However, the duration of this discount phase deserves attention.

Since early February 2026, price has traded below both the active investor cost basis and the recent buyer breakeven level for approximately five months, making this one of the more extended deep value episodes in Bitcoin's history.

Prolonged accumulation at such a discount, where new capital is consistently deployed below the cost basis of both recent buyers and the broader active market, has conventionally served as the foundation for cyclical bottoms and represents an attractive zone for value-oriented investors.

While the evidence suggests this process is approaching its later stages, the lower band of the bear market range near the Realized Price at $53k remains a possibility that cannot be dismissed.

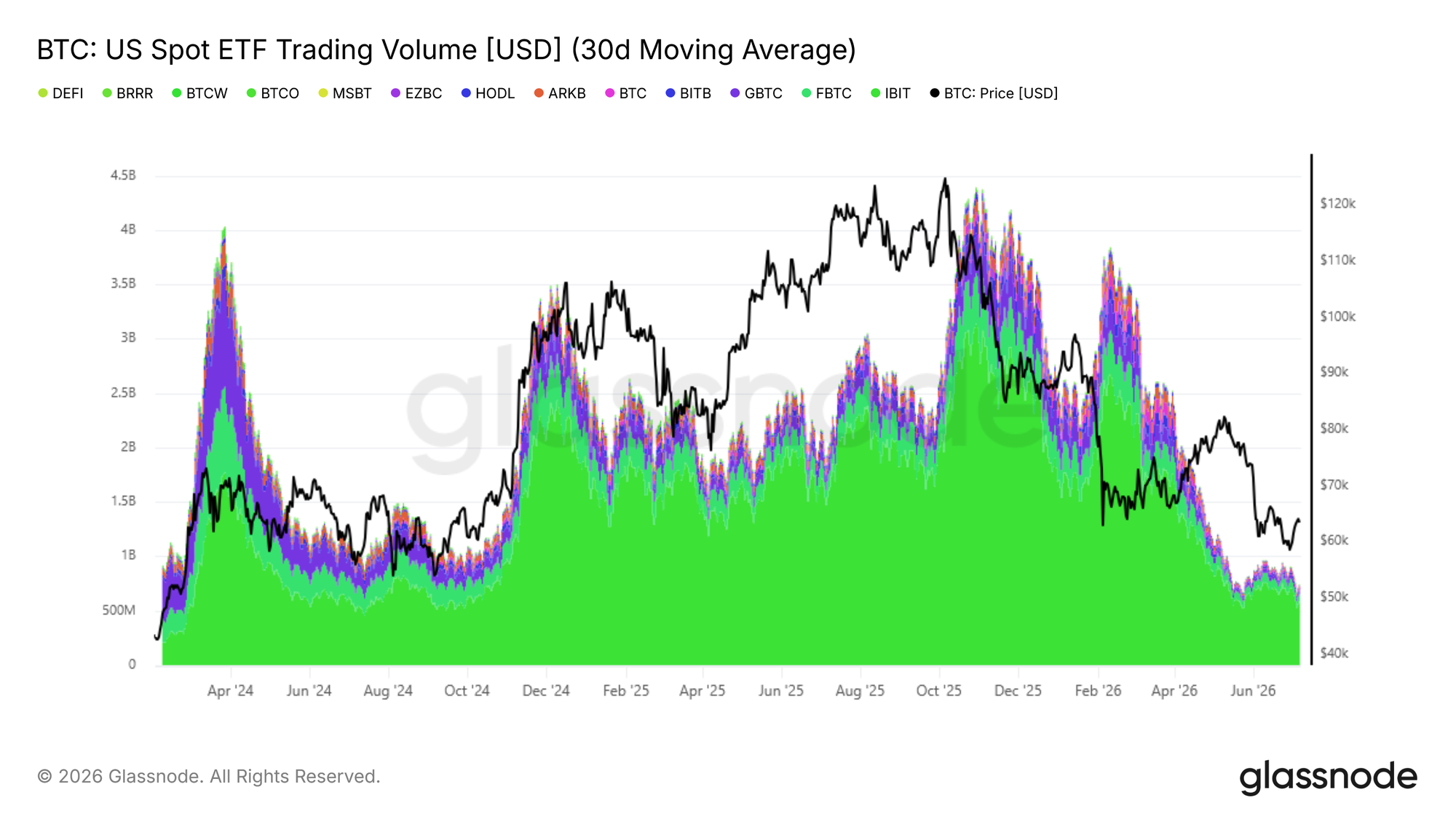

4. ETF OUTFLOWS

ETF investors provides a complementary lens on institutional demand. The 30-day SMA of ETF Netflow captures the smoothed daily net capital entering or leaving US spot Bitcoin ETFs, filtering out single-day volatility to reveal the underlying trend in institutional positioning.

Since mid-May 2026, this indicator shifted into a net monthly outflow regime, peaking at -$193M per day in early June before cooling to -$88.9M per day currently.

Alongside net flows, the US Spot ETF Trading Volume provides a complementary read on whether institutional confidence is recovering. The 30-day SMA of daily ETF trading volume has been ranging between $650M and $950M per day, a level comparable to the Q4 2024 environment and the same time ~80% below the $4.4B per day peak recorded in October 2025.

While the current volume range reflects baseline institutional participation, it remains deeply muted relative to bull market peaks, indicating that conviction among ETF investors has not meaningfully returned.

A sustained expansion in daily trading volume alongside a compression of net outflows would together constitute the minimum conditions for confirming a revival in institutional demand. Until both signals emerge in tandem, the off-chain data continues to reinforce the broader bearish regime identified through on-chain metrics.

5. OPTIONS MAX PAIN

Beyond positioning and skew, the relationship between spot and options market structure adds further context. Bitcoin trades about 6% below its aggregated max pain of $66k, the strike where the most open interest expires worthless and toward which price often gravitates into expiry.

The discount has widened with this week's drop, but it remains far from the deep stress observed during February's selloff, sitting nearer the middle of a range that has characterized most of 2026.

Max pain has functioned as a loose gravitational anchor throughout the year, with spot oscillating around it rather than sustaining prolonged deviations. A sustained reclaim of $66k would shift the near-term read constructive, while a further widening would reinforce the defensive positioning evident across the options surface.

Conclusion

Across all three layers of analysis, the market presents a consistent picture of a bear market in its later stages. On-chain, the five-month deep value regime and rising long-term holder capitulation at $280M per day confirm that supply redistribution is underway, though a sustained cooldown in this metric remains the prerequisite for a credible transition.

Off-chain, ETF outflows have eased from their June peak but continue to bleed on a monthly basis, while trading volume at roughly 80% below October 2025 levels reflects muted institutional conviction. In derivatives, positioning has leaned cautiously long with the put/call ratio at its 2026 low, yet the skew and vol surface still price meaningful downside risk.

Taken together, the conditions for a bottoming process are in place, but the confirmation signals have not yet arrived. The market requires further cooling in capitulation pressure, stabilization in institutional flows, and ideally a sustained reclaim of the True Market Mean before the probability of a regime transition can be weighted constructively.

#BTC #Crypto #Cycle #bottom #onchain